When a pharmacist hands you a bottle of generic lisinopril instead of the brand-name Zestril, it’s not just a simple swap. Behind that decision is a complex financial system that determines whether the pharmacy makes money, whether you pay less at the counter, and whether the system as a whole saves money-or just shifts costs around. Generic substitution is supposed to cut costs. But in practice, how pharmacies get paid for those generics can make all the difference.

How Pharmacies Get Paid for Generics

Pharmacies don’t just sell drugs at retail. They’re reimbursed by insurance plans, Medicare, Medicaid, and Pharmacy Benefit Managers (PBMs). The way they get paid for a generic drug isn’t straightforward. There are three main models: cost-plus, Maximum Allowable Cost (MAC), and fixed dispensing fees.Cost-plus reimbursement means the pharmacy gets paid the actual price they paid for the drug, plus a fixed percentage or flat fee. It sounds fair, right? But here’s the catch: if the pharmacy bought the generic for $2, and the reimbursement rate is 120% of cost plus a $5 dispensing fee, they get $7.40. That’s fine if the drug stays cheap. But if the cost jumps to $5 because the manufacturer raised prices, the pharmacy gets $11. That’s more money-but it doesn’t mean the patient pays less. The payer (insurance or Medicare) is footing the bill.

Most commercial plans and PBMs use MAC lists instead. These are lists of the maximum amount a plan will reimburse for a generic drug. For example, a MAC for 30 tablets of generic metformin might be $4. But here’s the problem: MAC lists aren’t standardized. One PBM might set the MAC at $3.50, another at $5.20. And pharmacies rarely know how those numbers are calculated. Sometimes they’re based on wholesale prices from months ago. Sometimes they’re pulled from data that doesn’t reflect real-time costs. That means a pharmacy might buy a generic for $3.20, but get reimbursed $4. That’s a 25% profit. But if the MAC drops to $3, they lose money.

And then there’s the dispensing fee. This is the flat fee pharmacies get just for filling the prescription-usually $5 to $12. It’s meant to cover labor, packaging, and overhead. But when reimbursement for the drug itself drops, that fee becomes the pharmacy’s only reliable income. Many independent pharmacies now rely on that fee more than the drug margin. That’s why some pharmacies push for higher-volume, lower-margin generics. It’s not about profit per pill-it’s about staying open.

Why PBMs Favor Certain Generics

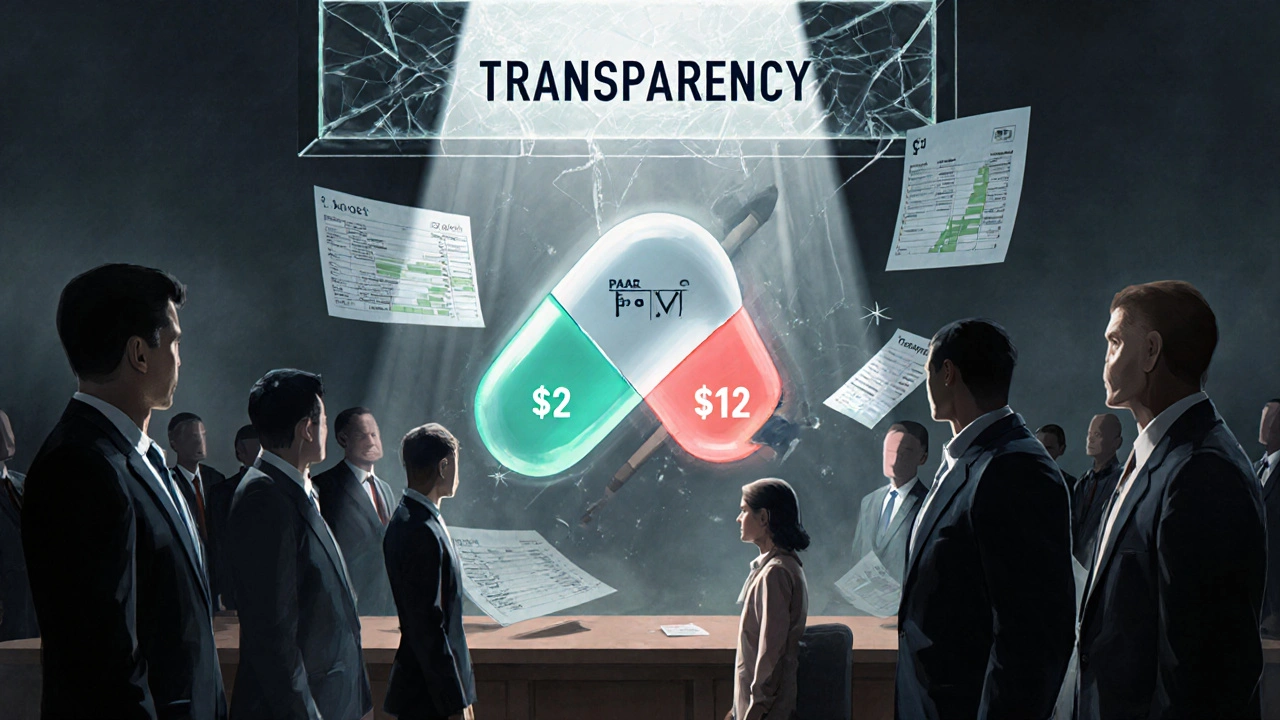

Pharmacy Benefit Managers (PBMs) control about 80% of prescription claims in the U.S. through CVS Caremark, Express Scripts, and OptumRx. They negotiate drug prices between manufacturers and insurers. But their business model isn’t always aligned with saving money for patients.One major issue is spread pricing. PBMs tell the pharmacy they’ll pay $4 for a generic. But they charge the insurance plan $12. The $8 difference is their profit. That’s spread pricing. And here’s the twist: they don’t have to tell the plan or the patient what the real cost is. So if a cheaper generic exists-say, one that costs $1.50-the PBM can still put the $10 generic on the formulary. Why? Because the spread is bigger. The pharmacy still gets paid $4. The patient pays the same copay. But the PBM pockets $8 instead of $1.50.

Research shows this isn’t theoretical. In one study, generics substituted within the same therapeutic class had prices 20.6 times higher than their cheapest alternatives. Even when it was the same drug with a different dosage form-like switching from a tablet to a capsule-the price difference was 20.2 times. But if it was the same manufacturer’s generic, the price difference was only 1.4 times. That tells you something: PBMs aren’t choosing based on cost. They’re choosing based on how much profit they can make.

And it’s not just about the drug. PBMs use something called Generic Effectiveness Rates (GERs). These are contracts that cap how much they’ll pay for generics over a period. If a pharmacy dispenses too many high-cost generics, the PBM might penalize them. But if the pharmacy sticks to high-margin generics, they get rewarded. So the incentive isn’t to save money-it’s to hit the PBM’s profit targets.

What This Means for Pharmacies

The financial pressure on pharmacies is real. Gross margins on generic drugs average 42.7%, compared to just 3.5% for brand-name drugs. That sounds great-until you realize that the margin depends entirely on the reimbursement model. If the MAC drops, or if the PBM changes the formulary overnight, that margin can vanish.Independent pharmacies are being squeezed. Between 2018 and 2022, more than 3,000 closed. Why? Because they couldn’t compete with big chains that get better reimbursement rates through volume deals. Chains negotiate lower MACs and higher dispensing fees. Small pharmacies? They’re stuck with whatever the PBM gives them.

Some pharmacies try to offset losses by pushing higher-margin drugs. But that’s risky. If a patient needs a low-cost generic and the pharmacy doesn’t stock it because it’s not profitable, the patient might not fill the prescription at all. That’s not just a financial problem-it’s a health problem.

And it’s not just about generics. When reimbursement rates drop too low, pharmacies stop carrying specialty drugs-like those for diabetes or rheumatoid arthritis-because they can’t afford to tie up cash in expensive inventory. That delays treatment. Patients go without. Pharmacies lose trust. And the system loses.

Therapeutic Substitution: The Real Savings Opportunity

Most people think generic substitution means swapping a brand-name drug for its generic version. But the biggest savings come from therapeutic substitution-switching to a different generic drug in the same class that’s cheaper.For example, instead of prescribing lisinopril, a doctor might switch a patient to enalapril, which costs half as much. Or instead of metformin ER, switch to regular metformin. These aren’t just generics-they’re different drugs with the same clinical effect.

The Congressional Budget Office found that in 2007, switching brand-name drugs to cheaper generics in just seven Medicare drug classes saved $4 billion. But switching one generic to another cheaper generic? Only $900 million. Why? Because the system doesn’t encourage it. PBMs don’t reward therapeutic substitution. Pharmacists aren’t trained to suggest it. Doctors don’t know the price differences.

And here’s the kicker: patients often don’t know either. They assume “generic” means “cheapest.” But it doesn’t. A $10 generic isn’t cheaper than a $2 generic. Yet both are labeled “generic.” The difference? The PBM’s spread.

What’s Changing? Regulation and Transparency

There’s growing pressure to fix this. The Federal Trade Commission (FTC) launched investigations in 2023 into PBM spread pricing and MAC list secrecy. They’re asking: Why aren’t payers told what the real drug cost is? Why are MAC lists hidden?The Inflation Reduction Act of 2022 forced Medicare Part D to disclose drug prices. That’s a start. But it doesn’t yet apply to commercial insurance. Prescription Drug Affordability Boards (PDABs) in 15 states are now setting Upper Payment Limits (UPLs) for drugs. If a generic costs more than the UPL, the plan won’t cover it. That forces PBMs to use cheaper alternatives.

But there’s resistance. PBMs argue that transparency will reduce competition and raise prices. But data shows the opposite. When states like Minnesota and California made MAC lists public, generic prices dropped. Pharmacies started stocking cheaper options. Patients paid less. PBMs still made money-but not through hidden spreads.

What Patients and Pharmacies Can Do

Patients have more power than they think. Ask your pharmacist: “Is there a cheaper generic option?” Don’t accept “this is what’s on your plan.” Ask for the price without insurance. Ask if they can order a lower-cost version. Many pharmacies can get it within a day.Pharmacists need to be advocates. Track the real cost of generics you dispense. Know your MAC rates. Push back when PBM formularies favor high-cost generics. Document when patients can’t afford their meds because of reimbursement policies. Report it to state pharmacy boards. These systems only change when people speak up.

And pharmacies? If you’re independent, consider joining a group purchasing organization (GPO). These groups negotiate better drug prices and reimbursement rates collectively. You can’t fight PBMs alone. But together, you can.

The goal of generic substitution is simple: make medications affordable. But right now, the system rewards complexity over clarity. It rewards profit over savings. Until reimbursement models change-until MAC lists are transparent, until spread pricing is banned, until pharmacists are paid fairly for helping patients choose the right drug-then the promise of generics will remain unfulfilled.

How does generic substitution affect my pharmacy’s profits?

It depends on how you’re reimbursed. If you’re paid under a cost-plus model, your profit is tied to the drug’s acquisition cost. If the generic price drops, your profit drops too. With MAC lists, you might make more if the MAC is higher than your cost-but PBMs often set MACs just above what they pay manufacturers, not what you pay. Dispensing fees are your safest income, but they’re shrinking as PBMs cut them to control costs.

Why do some generics cost more than others?

It’s not about quality-it’s about pricing strategy. PBMs put higher-priced generics on formularies because they create bigger spreads. A $12 generic might be reimbursed at $15, giving the PBM a $3 spread. A $2 generic might only give them $0.50. So even if the $2 version is just as effective, the PBM pushes the $12 one. Pharmacies get paid the same either way, so they fill what’s on the list.

Can I ask my pharmacist for a cheaper generic?

Yes, and you should. Ask: “Is there a different generic version of this drug that costs less?” Pharmacists have access to drug pricing databases and can often find alternatives. Sometimes they can even order it in. Don’t assume your copay is fixed-ask for the cash price too. It’s often lower than your insurance copay.

Why are independent pharmacies closing?

Because reimbursement rates have dropped while operating costs rose. PBMs control most of the market and set low MACs and dispensing fees. Independent pharmacies can’t negotiate like big chains. Many now operate on less than 1% profit per prescription. When a single drug’s reimbursement drops by $1, it can mean losing hundreds of dollars a month. Over time, that’s not sustainable.

Does generic substitution always save money?

Not always. If the system rewards high-cost generics through spread pricing, then switching to a different generic might not save anything. True savings come from switching to the lowest-cost therapeutic alternative-not just any generic. But without transparency, patients and providers can’t make those choices. The system is designed to hide the real cost.

Derron Vanderpoel

November 20 2025bro the PBM thing is wild. i got a $12 generic for my blood pressure med last week, paid $5 copay, then saw the cash price was $2.50. they didn’t even tell me. i felt like i got scammed by the system.